Let's talk about Ethereum

Let's take a look at its tokenomics, recent and upcoming changes, and why Ethereum is not shaping up to be sound money.

Since some in the Ethereum community believe it may become a sound money, it's prudent to make the comparison to a cryptocurrency well-known for its tried and true, well-understood monetary issuance model. This, of course, is Bitcoin. It may seem unfair or inappropriate to compare a money meant as an infallible store of value to one that was originally intended to solve a much smaller problem than, well, all of money… But this can of worms has already been opened by Vitalik Buterin himself.

Some are expecting a “flippening” thanks to Ethereum’s newfound (occasionally) deflationary tokenomics. However, they might be forgetting that market cap (as meaningless as such a metric might be) is calculated as price times supply, and shrinking supply alone does not make for a higher market cap. Further, a large part of Bitcoin’s value comes not just from its scarcity or high stock-to-flow ratio, but also, its dependability. It is a much more known quantity than the constant experiments put forth by the Ethereum Foundation. Lyn Alden dives into this in her excellent piece, An Economic Analysis of Ethereum. Turns out, scarcity of supply alone does not a sound money make.

One could also make the argument that ETH 2.0, by building inflation into the protocol, could worsen the already-suspect Gini coefficient of Ethereum (with the vast majority of wealth in the hands of the few), which Vitalik does his best to trivialize the importance of which in his article, Against overuse of the Gini coefficient. It’s hard to think of a more privileged take on the subject of wealth inequality. The supply is uncapped, much like the current system of the petrodollar, and as such, there is no limit to how much wealth can be accumulated by Ethereum whales.

Meanwhile, Bitcoin, and its hard monetary limitations set in stone since its inception, can endure few monetary shenanigans for very long. Bitcoin-facing derivatives markets, while still somewhat impactful, are not as highly leveraged as, say, fractional reserve banks, or nation states. Further, if Bitcoin does become the global monetary standard, Bitcoin whales will eventually be forced to spend their bitcoin to meet financial obligations payable only in bitcoin, and as such, they may never have to trade their sound money for dirty government-money. As bitcoin is spent and the Bitcoin Economy grows, it becomes more distributed around the world. Also of note, the Bitcoin transfer volume this year could outpace the entire GDP of the United States.

As for Ethereum, Tomer Strolight outlines a number of problems of fairness, inequality, community exploitation, an adversarial approach to supporters, and a never-ending string of broken promises in his insightful article, The Problem with Ethereum. It should give some background on why, from a Bitcoiner’s perspective, Ethereum’s approach to all of these things has been reprehensible, and not only contrary to the principles the Bitcoin community holds, but undermines the very value proposition of the concept of decentralized, cryptocurrency in the first place.

Bitcoin is meant to be an egalitarian protocol, where the bankers on Wall St. have to play by the same rules as the people on Main St., to the lobbyists on K Street, to the farmers in El Salvador. Nobody gets preferential treatment from Bitcoin. However, by introducing staking into the protocol, in addition to burning the base fee, as introduced with EIP 1559 in the recent London fork, the dynamics of the Ether token aren’t all that much different than the current, unfair system. A system where there are those who are privileged to have the majority of their money in investments, and then there are those who simply have bills to pay and have money sitting idle in their bank accounts, perpetually fated to have weaker purchasing power through protocol-driven dilution. And thus, the rich get richer, and the poor get poorer, at least, with Ethereum 2.0, with its two kinds of money: staked Ether, which provides interest, and unstaked Ether, which gets diluted by interest from the former. It’s sort of a decentralized Cantillon effect, remarkably enough.

While Bitcoin’s present volatility can be an issue, as it grows, the magnitude of the issue lessens a great deal with each halving cycle, as an analysis by Ecoinometrics shows in their article about Bitcoin’s Volatility squeeze. Let’s also remember: the reason Bitcoin is so volatile against fiat currency is, more Bitcoin cannot be made to satisfy demand, so, it exhibits an inelasticity of supply when measured against a money manipulated by central banks, in addition to efficiency losses from foreign exchange markets converting money between nation states. Bitcoin might be considered a more reliable way to measure scarcity in the context of the global market in addition to local markets, and as such, could be a better mechanism to distribute scarce resources, i.e., to back a functioning global economy with a money controlled by no single nation that can manipulate the money in its favor.

Arguably, much of Ethereum’s value could simply be a result of the fact that it is highly correlated with Bitcoin’s price performance. Bitcoin aims to be a store of value, Digital Gold, while Ethereum’s tokenomics generally used to resemble that of a commodity with a low stock-to-flow ratio, a Digital Oil of sorts. However, if it enters an era when new blocks would be added solely through the Proof of Stake mechanism, GPU miners may one day be no longer needed. This supports an ESG (Environmental, Social, and Governance) narrative that would be more akin to a Digital Biofuel than a legitimately “green” substitute. One reason for this analogy is that, biofuels often are less efficient than their supposedly “dirty” alternatives. Likewise, if a vast system of cloud-supported validator nodes and the blockchain chandelier of 64 shard chains are implemented to their intended fullest extent, Ethereum will require an enormous amount of cloud computing, more so than it already does through Web3-focused services like Infura. Cloud computing is notorious for being energy-hungry, and its energy usage equals and possibly exceeds that of Bitcoin’s or Ethereum’s. An older figure for datacenter global yearly electrical consumption is 205 TWh/yr back in 2018, according to this article, The Bitcoin Energy Debate: Lessons from the Data Center Industry. Contrast this with similar, more recent figures for Bitcoin and Ethereum, as provided by Digiconomist, which is not known for being a source sympathetic to cryptocurrency mining.

As one can see, if numbers are compared, cloud computing uses as much, if not more energy than cryptocurrency mining. Interestingly enough, there are actually many ways Bitcoin miners can have a positive impact on energy production. One example is that they can co-locate near power plants, and use their excess capacity in absence of grid demand, while also avoiding transmission and power conversion losses, all thanks to Bitcoin’s flexibility and capability to tolerate intermittent consumption. Bitcoin could prove to be the “buyer of last resort” for energy sources that cannot find other buyers, which could prove to make renewable energy projects such as the ones proposed in El Salvador more economically viable at the outset. For more examples and context on why Bitcoin mining could actually be quite helpful towards accelerating the transition to renewable energy, and lessening impact on our environment, be sure to read Lyn Alden’s excellent article on that subject, Bitcoin’s Energy Usage Isn’t a Problem. Here’s Why. Not everyone might care about the ESG narrative, but it’s important to acknowledge concerns and break down barriers to adoption caused by blatant misinformation spread by the mainstream media.

Further, with the exodus of Bitcoin miners from the notoriously-dirty Xinjiang province (and the seasonal, slightly more environmentally-sustainable presence in southern China), the geographic decentralization of hashrate comes with an added benefit of reduced dependence on fossil fuels by locating to nations with a more diverse energy mix. Roughly 70% of China’s energy comes from coal power plants.

Getting back to Ethereum, two common arguments critics make are, one, to point out the DAO hack, where Vitalik Buterin and the Ethereum Foundation seemingly— unilaterally— decided which fork to use as the main Ethereum chain. This is from a purportedly decentralized, permissionless, and public network. There’s been enough written on this point that this article won’t spend much time on it, other than to mention that it is a serious compromise to the primary value proposition that cryptocurrencies were meant to provide, in a way that no other thing made by humans can: a system of currency resistant to manipulation by any single party, no matter their capability for outsize impact. I’m sure people who’ve been in the Ethereum community are tired of hearing this argument, and might roll their eyes when this criticism and others are mentioned, but it’s important to acknowledge criticisms and understand why they exist.

The second argument critics often point to is the “70% premine”. This is not quite accurate, however, since that is taking into account its present supply of roughly 117 million ETH at the time of writing. However, as Ethereum went live in 2014-2015, 100% of the Ether supply was pre-mined. At least 72 million ETH wound up in the pockets of launch investors, the Ethereum Foundation, and core team members. This is detailed in a comprehensive piece written by Camila Russo, Sale of the Century: The Inside Story of Ethereum’s 2014 Premine.

Where Satoshi Nakamoto is not known to have sold a single bitcoin, since it was practically worthless at the time he distanced himself from the community in December 2010, Vitalik Buterin used his Ether for his own personal gain. The SEC might have a few bones to pick on that front. Gary Gensler, chair of the U.S. Securities and Exchange Commission— for what his opinion is worth— has mentioned on a few occasions that Bitcoin is more akin to a commodity than a security, whereas Ethereum might actually be a non-compliant security. Indeed, it’s hard to argue that Ethereum is decentralized enough to not personally benefit its founders, which are ever-present and financially rewarded on a regular basis from their involvement, perhaps meeting the Howie Test used to determine whether an investment is a security. This could pose an existential threat to the currency, if it were to be eventually delisted, or heavily regulated, in markets in which it is traded.

So, as speculators on Wall St. continue to inflate the prices of commodities through reckless speculation on government-guaranteed junk bonds, among other factors, we begin to enter an “everything bubble”, and a situation manifests where, if professional speculators call the top of the bubble and it doesn’t burst, they could lose their jobs. And so, they don’t call the top, and it’s unclear when the boom will become the inevitable bust. Could be tomorrow, or could be till hyperinflation becomes too obvious to ignore. And there is one cryptocurrency that has dynamics familiar to banks thriving within the current rigged system, whereas there is one that stands against them.

Meanwhile, widespread adoption of the Lightning Network continues to prove an inspiration to all who wish the good money to replace the bad money. From a humanitarian standpoint, it promises to help provide banking facilities to the 70% of Salvadorans who are unbanked. Since Bitcoin requires reliable availability of internet and electricity, while also serving as a means to bootstrap financial infrastructure in economies in developing nations, it could serve as a powerful incentive to accelerate the process of connecting billions of individuals all around the world to the global economy. For more on mass adoption, check out this recent article on how Lightning adoption is propelling Bitcoin usage in El Salvador, and beyond.

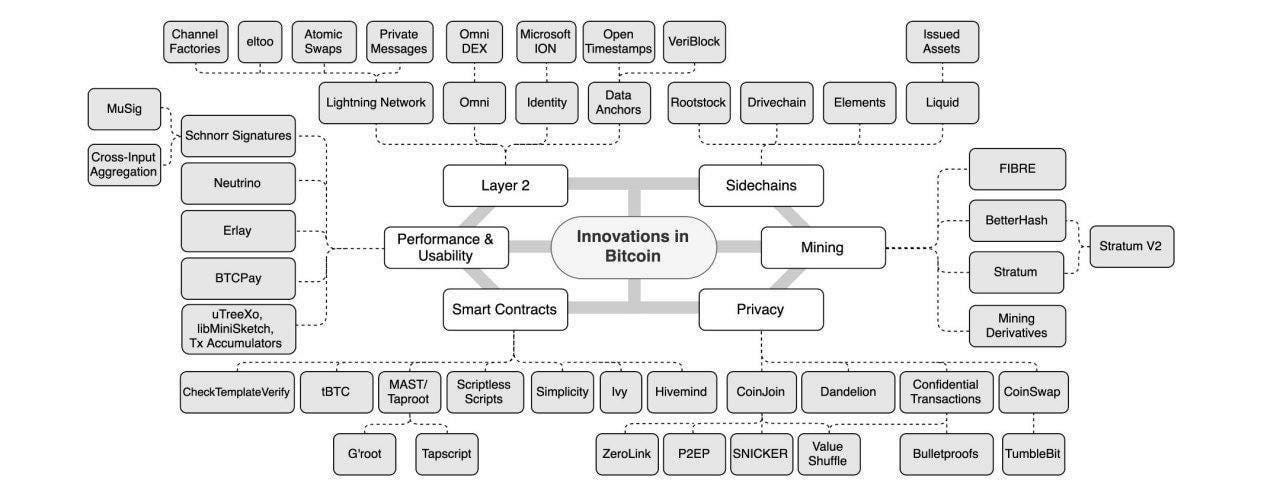

Are there things Ethereum can do that Bitcoin can’t? Sort of. But not all the problems those things aim to solve need to be solved in that way. Ethereum can result in hidden organizational centralization, even if it’s a Decentralized Autonomous Organization (DAO). Something or someone, somewhere, has to use keys to sign a transaction to deploy a smart contract. Some smart contracts feature token migration or burning, which allows organizations or individuals to change code or move funds without their token holder’s permission. Meanwhile, things like Lightning Network act as a truly decentralized protocol, with peer-to-peer state channels and operate in exclusion to the rest of the network while providing cryptographic guarantees against double-spend. These rules that are well-defined, reasonably secure, and beginning to be battle-tested. So, while Ethereum allows developers to roll their own rules, Lightning makes certain guarantees as to how tokens are transferred on the network. For example, while NFTs aren’t really possible on Lightning due to absence of global state, fungible tokens are possible, such as the “colored sats” developed by the very promising RGB project. RGB pioneers client-side validation, which results in greater decentralization, permissionlessness, and trustlessness. Despite claims to the contrary, the Bitcoin community is actually quite technologically innovative. However, Bitcoin’s fundamentals must be sound for projects built upon it to succeed. And much as TCP/IP is implicitly included in discussions around the web, all of Bitcoin’s layers should also be included in discussions around projects built within its ecosystem, since they share a common protocol, much as any project built on the Internet does.

This then challenges the assumption that ETH 2.0 will be reliably deflationary— if Ether is consistently spent on-chain, and if L1 smart contracts are written to. However, not only do scalability measures such as side-chains and rollups undermine that factor, if fees prove to be too high for too long, developers will look into switching their dapps to being based upon cheaper, more scalable techhnologies, such as platforms built on Lightning. With over 15,000 nodes and hundreds added every month, and each node theoretically capable of between 10-1000 transactions per second depending on node hardware (from budget ARM single board computers and virtualized cloud servers, to full-fledged baremetal servers) and also software (LND can be tuned to scale to 1000 TPS on commodity cloud servers), it’s conceivable that millions of transactions per second could be performed over the network, if not now, then in the very near future. With Lightning and, in the future, Lightspeed micropayments, Bitcoin’s scalability well into the future is all but assured. And the best part is that the fees aren’t burned, but provided to those who are doing work to help to scale the system, fueling its capability to grow. If fees prove to be too high on L2, there will be demand for L3 systems. And thus, Bitcoin behaves not only like a layered money like the existing financial system, but also, similarly to how HTTP is a network infrastructure layer on top of TCP/IP, thus lending substance to the analogy that Bitcoin can be considered “the internet of money”.

At which point, Ethereum’s promise of a utility as “Web3” fails to deliver, no matter the catchy names, developer adoption, and ICO money. Because, in the end, the users will go where there is the least friction. And if adoption falters due to competition from more innovative platforms, Ethereum cannot be guaranteed to be deflationary, whereas Bitcoin makes a protocol-level guarantee that supply will decrease by half every 210,000 blocks (roughly four years, given that slightly more than a thousand blocks are mined per week— 52 weeks * 4 years * 1000 blocks per week = ~210,000). And it’s those supply guarantees are what ordinary people, developers, institutions, and governments need to be confident in its capability to be a reliable store of value, medium of exchange, and unit of account, to power the economy of the future.

With all these factors considered, Bitcoin’s impact on the world could be much more positive and profound than the mainstream media is paid to make us believe. Meanwhile, no matter its recent and upcoming changes, it remains doubtful that Ethereum will have a similar impact anytime soon, and instead, is fated to continue to ride the coattails of Bitcoin, and all the financial, social, and technological innovation it brings.

If you liked this article, be sure to subscribe for easy access to future newsletters, and see my last article on why Bitcoiners claim that it’s the Best Money. Also, apologies to those who follow this for its purported focus on Rust. We’re getting there. It’s important, however, to appreciate the principles and impact of the technologies some of us might be working with.